kstest

One-sample Kolmogorov-Smirnov test

Description

h = kstest(x)x comes

from a standard normal distribution, against the alternative that

it does not come from such a distribution, using the one-sample

Kolmogorov-Smirnov test. The result h is 1 if

the test rejects the null hypothesis at the 5% significance level,

or 0 otherwise.

h = kstest(x,Name,Value)

Examples

Test for Standard Normal Distribution

Perform the one-sample Kolmogorov-Smirnov test by using kstest. Confirm the test decision by visually comparing the empirical cumulative distribution function (cdf) to the standard normal cdf.

Load the examgrades data set. Create a vector containing the first column of the exam grade data.

load examgrades

test1 = grades(:,1);Test the null hypothesis that the data comes from a normal distribution with a mean of 75 and a standard deviation of 10. Use these parameters to center and scale each element of the data vector, because kstest tests for a standard normal distribution by default.

x = (test1-75)/10; h = kstest(x)

h = logical

0

The returned value of h = 0 indicates that kstest fails to reject the null hypothesis at the default 5% significance level.

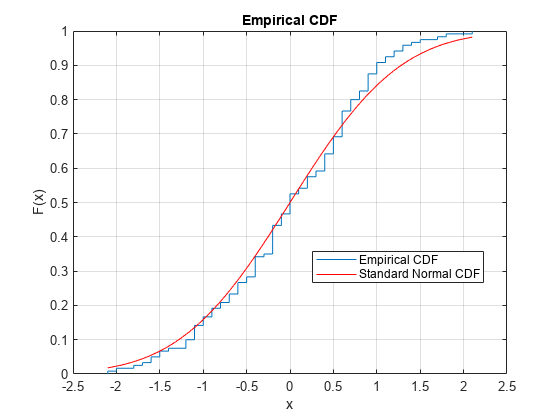

Plot the empirical cdf and the standard normal cdf for a visual comparison.

cdfplot(x) hold on x_values = linspace(min(x),max(x)); plot(x_values,normcdf(x_values,0,1),'r-') legend('Empirical CDF','Standard Normal CDF','Location','best')

The figure shows the similarity between the empirical cdf of the centered and scaled data vector and the cdf of the standard normal distribution.

Specify the Hypothesized Distribution Using a Two-Column Matrix

Load the sample data. Create a vector containing the first column of the students’ exam grades data.

load examgrades;

x = grades(:,1);Specify the hypothesized distribution as a two-column matrix. Column 1 contains the data vector x. Column 2 contains cdf values evaluated at each value in x for a hypothesized Student’s distribution with a location parameter of 75, a scale parameter of 10, and one degree of freedom.

test_cdf = [x,cdf('tlocationscale',x,75,10,1)];Test if the data are from the hypothesized distribution.

h = kstest(x,'CDF',test_cdf)h = logical

1

The returned value of h = 1 indicates that kstest rejects the null hypothesis at the default 5% significance level.

Specify the Hypothesized Distribution Using a Probability Distribution Object

Load the sample data. Create a vector containing the first column of the students’ exam grades data.

load examgrades;

x = grades(:,1);Create a probability distribution object to test if the data comes from a Student’s distribution with a location parameter of 75, a scale parameter of 10, and one degree of freedom.

test_cdf = makedist('tlocationscale','mu',75,'sigma',10,'nu',1);

Test the null hypothesis that the data comes from the hypothesized distribution.

h = kstest(x,'CDF',test_cdf)h = logical

1

The returned value of h = 1 indicates that kstest rejects the null hypothesis at the default 5% significance level.

Test the Hypothesis at Different Significance Levels

Load the sample data. Create a vector containing the first column of the students’ exam grades.

load examgrades;

x = grades(:,1);Create a probability distribution object to test if the data comes from a Student’s distribution with a location parameter of 75, a scale parameter of 10, and one degree of freedom.

test_cdf = makedist('tlocationscale','mu',75,'sigma',10,'nu',1);

Test the null hypothesis that data comes from the hypothesized distribution at the 1% significance level.

[h,p] = kstest(x,'CDF',test_cdf,'Alpha',0.01)

h = logical

1

p = 0.0021

The returned value of h = 1 indicates that kstest rejects the null hypothesis at the 1% significance level.

Conduct a One-Sided Hypothesis Test

Load the sample data. Create a vector containing the third column of the stock return data matrix.

load stockreturns;

x = stocks(:,3);Test the null hypothesis that the data comes from a standard normal distribution, against the alternative hypothesis that the population cdf of the data is larger than the standard normal cdf.

[h,p,k,c] = kstest(x,'Tail','larger')

h = logical

1

p = 5.0854e-05

k = 0.2197

c = 0.1207

The returned value of h = 1 indicates that kstest rejects the null hypothesis in favor of the alternative hypothesis at the default 5% significance level.

Plot the empirical cdf and the standard normal cdf for a visual comparison.

[f,x_values] = ecdf(x); J = plot(x_values,f); hold on; K = plot(x_values,normcdf(x_values),'r--'); set(J,'LineWidth',2); set(K,'LineWidth',2); legend([J K],'Empirical CDF','Standard Normal CDF','Location','SE');

The plot shows the difference between the empirical cdf of the data vector x and the cdf of the standard normal distribution.

Input Arguments

Output Arguments

More About

Algorithms

kstest decides to reject the null hypothesis

by comparing the p-value p with

the significance level Alpha, not by comparing

the test statistic ksstat with the critical value cv.

Since cv is approximate, comparing ksstat with cv occasionally

leads to a different conclusion than comparing p with Alpha.

References

[1] Massey, F. J. “The Kolmogorov-Smirnov Test for Goodness of Fit.” Journal of the American Statistical Association. Vol. 46, No. 253, 1951, pp. 68–78.

[2] Miller, L. H. “Table of Percentage Points of Kolmogorov Statistics.” Journal of the American Statistical Association. Vol. 51, No. 273, 1956, pp. 111–121.

[3] Marsaglia, G., W. Tsang, and J. Wang. “Evaluating Kolmogorov’s Distribution.” Journal of Statistical Software. Vol. 8, Issue 18, 2003.

Version History

Introduced before R2006a

See Also

kstest2 | lillietest | adtest

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)